Are you interested in learning more about how Theta options are calculated? If so, then you're in the right place!

In this blog post, we'll go over the basics of Theta options and explain how they're calculated, from breaking down how factors such as time decay impact option pricing to exploring some specific formulas used to price these derivatives by the end of this article, you should have a solid understanding of what goes into calculating an option's Theta value.

So let's dive in and explore everything that goes into determining how much impact a single day can have on your portfolio with Theta Options.

Overview of Theta Options and Why They Are Important

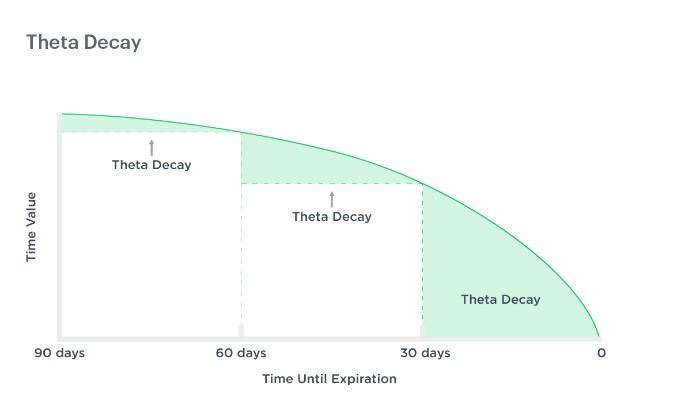

Theta, which measures the decay rate in an option's value over time, is a key component in options pricing. Theta is commonly referred to as the "time decay" or "rate of time decay"; it is used by traders and investors alike to value their options contracts and better manage their associated risks.

It is important to note that the decay rate is not linear, which will accelerate as we approach expiration. As a result, understanding how Theta options are calculated can help investors and traders better anticipate changes in option pricing leading up to expiration.

What Factors Influence Theta 0ption Calculations

The calculation of Theta options is a complex process; many factors influence the price of these derivatives.

Time decay

The most important factor is time decay, which measures the rate at which an option's value decreases over time. When calculating an option's Theta value, analysts will typically measure how much the option has decayed in a single day by considering interest rates, dividends earned, and other external factors.

volatility

Volatility can also impact the pricing of Theta options. Volatility refers to how unpredictable or erratic an asset's price movements can be; when it comes to options trading, higher levels of volatility often result in higher premiums for call-and-put options.

strike price

The strike price has a significant influence on Theta option calculations. When an option's strike price is close to the current market price of the underlying asset, it will usually be priced higher than if it is further away from the current market price. Thus, when determining the Theta value for an option, analysts will often consider its distance from the current market price.

Many factors can affect how Theta options are calculated and priced; understanding these concepts is essential for any investor who wants to make informed decisions about their trades and maximize their potential profits in this area of investing.

A Breakdown Of How Theta Values Are Calculated For Different Types Of Options

Theta values are calculated differently depending on the type of option you're looking at. Both calls and puts have different methods for determining their Theta values

.

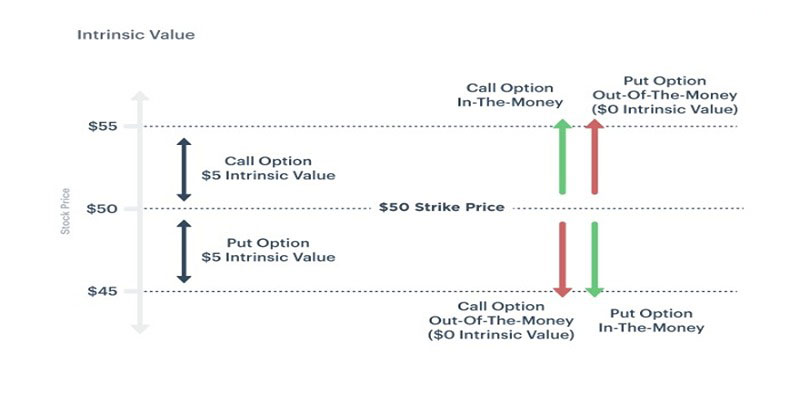

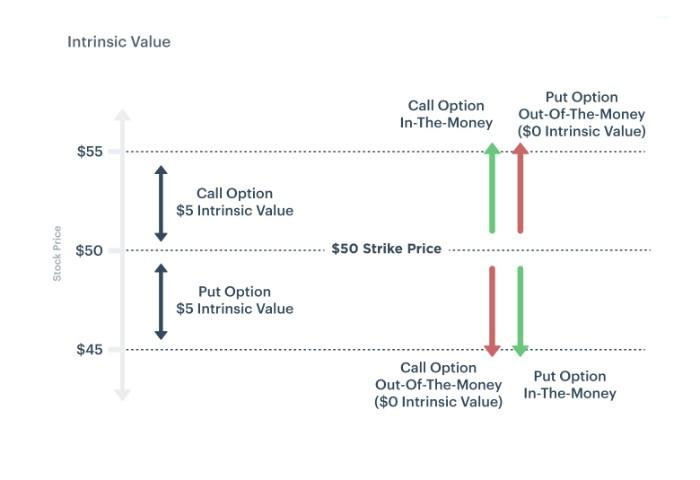

Call options' Theta value can be determined by subtracting the intrinsic value from the option's price and dividing it by the number of days until expiration. This shows how much time decay will affect the option's price over a certain period.

On the other hand, options consider both intrinsic value and implied volatility to determine their Theta values. Intrinsic Value is simply the current asset price minus strike price, while Implied Volatility helps to adjust pricing based on changes in expected stock moves.

Once the intrinsic value and implied volatility are factored in, the Theta value can be calculated by subtracting the intrinsic value from the option's price and then dividing that number by the option's time to expiration. This gives you a good idea of how time decay will affect your option's price over a certain period.

By exploring different types of options and understanding how their Theta values are determined, you can be sure to make the most informed decision when trading options. Knowing how much time decay will affect your option's pricing can help you decide whether or not a specific trade is right for you.

Illustrative Examples Of How To Calculate Theta For An At-The-Money Option, a Long Call Option, And a Short Put Option

First, let's look at calculating the Theta for an at-the-money option. An at-the-money option is one whose strike price equals the underlying asset's current market value. To find the Theta for this type of option, you'll need to know the current stock price and volatility and the remaining life of the option contract (also referred to as its time to expiration). Then you can calculate the Theta using this formula: Theta = (Stock Price x Volatility x Time to Expiration) / 365.

Next, let’s consider a long call option. This option gives you the right to purchase shares of a stock at an agreed-upon price in the future. To calculate its Theta, you must know the same data points for an at-the-money option and include the strike price. Then you can use this formula: Theta = (Stock Price - Strike Price x Volatility x Time to Expiration) / 365.

If you have a short put option, which grants someone else the right to sell shares of stock to you at an agreed-upon price, you’ll need to use a slightly different formula. Here it is: Theta = (Strike Price - Stock Price x Volatility x Time to Expiration) / 365.

By understanding how to calculate Theta for different options, you can make more informed trading decisions and better manage your portfolio’s risk.

Use Technology Tools To Automate Your Theta Option Calculations

Automating options calculations in today's fast-paced investment environment can save you time and energy. Luckily, technology tools are available to assist with this task. Using such tools can allow investors to quickly and accurately calculate the value of their Theta options without requiring manual input.

These tools typically require minimal setup and use algorithms or other sophisticated mathematical models to perform the necessary calculations in a fraction of the time it would take for an investor to do so manually. Many of these tools offer graphical displays which can help users understand how different factors affect the pricing of their Theta options in clear terms.

Utilizing technology tools is a great way to ensure accuracy when calculating Theta option values and save time. With the right tool, investors can quickly and easily determine how much impact a single day or certain market conditions can have on their portfolios.

These tools can help increase understanding of options pricing and provide insight into potential opportunities for investing based on calculated Theta option values.

FAQs

Is there a difference between American Options and European Options regarding Theta Options?

Yes, there is a difference between American and European Options when it comes to Theta Options. American options are more expensive than European options because they allow the option holder to exercise at any time before expiration.

In contrast, a European Option only allows the option holder to exercise on the expiration date. As such, an American option will have a higher Theta Value than its European counterpart since time decay will have a greater impact on its price.

What is the difference between a Theta and an option?

Theta is a measure of the time decay that influences the change in price for an option on a particular day. The actual option, however, represents the right to buy or sell a security at a pre-determined price (the strike price) within a certain period.

Are Theta options taxed?

Yes, Theta options are taxed. How much a trader will be taxed on their Theta options depends on the type of option they’re trading and the country they’re trading in.

Conclusion

Although figuring out how to calculate Theta Options may sometimes seem daunting, you can simplify it with the proper educational resources and technology tools. It is important to take the time to further your understanding of the subject to accurately price financial products and understand risk management strategies.