Are you concerned about taxation on non-qualified deferred compensation plans? As a business owner or executive, understanding how these complex plans are taxed is essential for managing your finances responsibly and getting the most from your investments.

In this blog post, we explore the key points of taxation on non-qualified deferred compensation plans so that you can make informed decisions and achieve financial security for yourself and your family. Read on to learn more!

Understanding Non-Qualified Deferred Compensation Plans

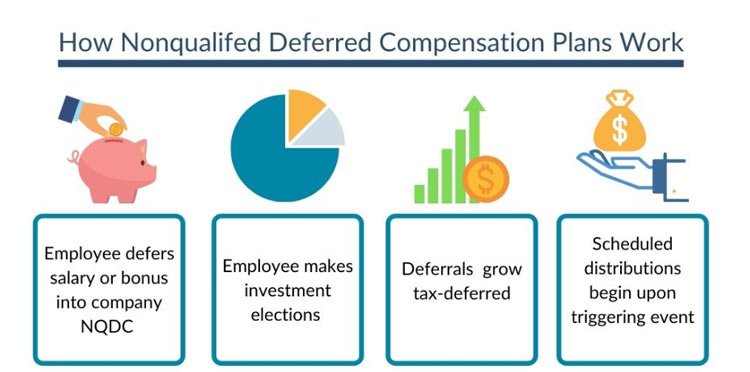

Non-qualified deferred compensation plans can be complicated, but understanding the taxation related to them is essential for financial security. These plans allow business owners and executives to defer a portion of their income until later years. This can provide significant tax benefits since taxes on the deferred income are not due until later. It's important to note that these plans may be subject to various taxes depending on how they are structured.

Income earned from non-qualified deferred compensation plans is generally considered taxable wages in the year earned and must be reported on the employee’s federal tax return. In addition, if an employee takes a lump sum distribution from the plan, he or she will likely owe additional taxes on this amount. Furthermore, these plans may be subject to additional Medicare tax or self-employment taxes as well as penalties for non-compliance with IRS regulations.

It's important to note that if an employee withdraws money from the plan before they are 59 ½ years of age, it can result in a 10% penalty fee on the withdrawal amount. It is also essential for employers to understand the taxation rules associated with their particular type of plan and comply with all applicable laws. For this reason, it is recommended to consult a qualified tax professional when considering a non-qualified deferred compensation plan.

Benefits of Deferring Compensation Under an NQDC Plan

One of the main benefits of deferring compensation under a non-qualified deferred compensation (NQDC) plan is that it can provide significant tax savings. When deferring income, employees are only required to pay taxes on the amount in later years. This allows them to save money by avoiding current taxes and instead pay them in future years when their tax rate may be lower. Additionally, NQDC plans allow employees to take larger distributions from their accounts than if they were paid out annually right away since fewer taxes will be due.

Furthermore, NQDC plans to provide flexibility for employers and employees regarding how funds are managed or used. For example, an employer may allow employees to direct their own investments in the plan or provide them with various investment options. Employees may also access funds from the plan for various purposes, such as college tuition payments or home purchases.

The additional flexibility and tax savings offered by NQDC plans make them an attractive option for employers and employees. As long as the rules associated with these plans are followed, and employers remain compliant with applicable laws, they can benefit everyone involved. It is important to note that it is always best to consult a qualified tax professional when considering an NQDC plan to ensure all regulations and requirements are met.

Tax Implications of Deferred Compensation

The tax implications of deferred compensation can vary depending on the type and structure of the plan. Generally, income earned from deferred compensation plans such as non-qualified deferred compensation (NQDC) plans are considered taxable wages in the year they were earned. This means that they must be reported on an employee’s federal tax return and may also be subject to various other taxes depending on how the plan is structured.

In addition to ordinary income taxes, an employee may owe additional taxes such as self-employment or Medicare taxes. Furthermore, if employees take a lump sum distribution from their NQDC plan before they reach age 59 ½, they may incur a 10% penalty fee on the withdrawal amount. Employers must understand the taxation rules associated with their particular type of deferred compensation plan and comply with all applicable laws.

Tax Strategies for Reducing the Tax Burden on NQDCs

Tax strategies for reducing the tax burden on non-qualified deferred compensation (NQDC) plans include taking advantage of certain deductions or other savings opportunities. For example, employees may defer a portion of their income into an NQDC plan and claim a deduction for this amount. This can help reduce the overall taxable income and thus lower the employee’s taxes. Additionally, employers may make pre-tax contributions to their employees' plans if allowed by the IRS.

Another strategy is to take advantage of ‘catch-up’ contributions which allow eligible individuals over 50 years old to contribute additional money each year without running afoul of contribution limits set by the IRS. Furthermore, employees can use the funds in their NQDC plan to invest in certain qualified investments, such as mutual funds or bonds, and potentially receive a tax break.

Tips for Managing Your Taxes Under an NQDC Plan

When managing taxes under a non-qualified deferred compensation (NQDC) plan, it is important to understand and follow applicable laws and regulations. This includes staying up-to-date with tax code changes and filing all necessary paperwork and forms on time. Additionally, taking advantage of certain deductions or incentives can help reduce taxes owed on NQDC plans.

Employees should consider deferring a portion of their income into an NQDC plan to receive a deduction for this amount. This can help lower their overall taxable income and thus reduce the total taxes due. Additionally, employers may make pre-tax contributions to their employees' plans if allowed by the IRS, lowering the employee’s overall tax burden.

Resources to Help You Understand NQDC Taxation

In addition to consulting a qualified tax professional for advice on the taxation of non-qualified deferred compensation plans, several resources are available online to help individuals understand the implications and rules associated with NQDCs.

The IRS website includes detailed information about various tax-related topics, including deferred compensation and filing taxes correctly and taking advantage of deductions or incentives.

FAQs

Q: What is taxation on non-qualified deferred compensation plans?

A: Taxation on non-qualified deferred compensation plans refers to the income taxes that are due on accrued benefits within a plan. This may include contributions from employers and employees and any associated investment earnings or gains. It’s important to note that taxation on these plans can vary based on individual circumstances and the type of plan in question.

Q: Are employer contributions taxable?

A: Yes, employer contributions to non-qualified deferred compensation plans are generally considered taxable income for the employee when they are received by the employee, regardless of when they were contributed to the plan.

Q: Are there any exceptions for taxation on non-qualified deferred compensation plans?

A: Generally, taxation on non-qualified deferred compensation plans depends on the individual plan and its associated rules. However, some exceptions may apply. Examples include tax deferral opportunities or additional contributions available to certain individuals based on their executive status within the company. Additionally, some plans may offer special provisions for hardship distributions or rollovers to Roth IRAs which can help reduce overall taxes owed.

Conclusion

Taxation on non-qualified deferred compensation plans can be complex, but this guide should help you better understand your options. It’s important to remember that tax rules and regulations are subject to change, so it's best to consult a financial advisor for up-to-date information and personalized advice. With the right plan, you can maximize your savings while keeping taxes at bay. Understanding taxation on these plans is one step toward achieving long-term financial security!